I.

London’s recent success as a global tech mecca clustered around internet giants’ headquarters, world-class research institutions, and start-up hotspots has been no secret in recent years. It is, in fact, regarded as an exemplar of how the suburban corporate campus model that has largely dominated the global landscape of scientific and technological innovation for the last five decades can be internalized and enmeshed within existing urban fabrics to foster economic growth and employment. Given the importance of these latter as indicators of urban success, it is no surprise that in the UK capital, and particularly since the global financial crisis of 2008, politicians, real estate developers and urban professionals alike have unequivocally embraced the shift from the suburban to the urban tech ecosystem aiding it with all kinds of incentives and reliefs (e.g. tax cuts, privileged planning procedures, etc.). Starting with former Prime Minister David Cameron’s endorsement of the Tech City Investment Organisation in 2010 (now Tech City UK) to turn a fraction of East London into a “world-leading technology cluster,” a vast quantity of initiatives led by both the Greater London Authority (GLA) and the Central government alike have been deliberately put in place to foster digital economies as primers for urban regeneration and infrastructural overhaul.1

As an industrial sector whose assets are predominantly immaterial, the impact of the so-called digital economy on governmental policy and city planning is as vast as it is overlooked—both in terms of the peculiar model of aggregation it nurtures and the infrastructural requirements it carries. This obliviousness is in part due to the heterogeneity of the sector, of which the definition is inherently fuzzy. While one may be inclined to strictly link the digital economy to tech industries and information technologies, at a governmental level the category includes components as varied as e-commerce and e-businesses (the trading of goods or services over computer networks such as the internet and its supporting infrastructure—hardware, software, telecoms) as well as life sciences and publishing and broadcasting businesses.2 Further, while we are very well accustomed to the spatial resolution of most of its constituent subsections (such as Silicon Roundabout in Old Street, the glass towers of London’s two Financial Districts, or the corporate citadels in White City and Knowledge Quarter), the powering facilities, telecommunication/storage systems and networks that make its presence in the urban fabric even possible are mostly inconspicuous. And yet, one need only to look at London’s recent urban developments and regeneration schemes to see how policy and fiber not only run parallel to one another, but also at commensurate speed.3

Ever since the 1980s, governmental measures have supported the prolific grounding of networked economies within the capital’s undersoil. As Andrew Blum explains, the establishment of Canary Wharf as one of the world’s leading clusters for global finance and the subsequent establishment of London’s Internet Exchange within the nearby Telehouse (“the Heathrow of Internet buildings”) are both contingent upon not just the government’s “zonification” processes and policies of economic deregulation, but their proximity to London’s main communications trunks beneath the nearby A13 motorway.4 This principle remains valid up until this day, such that to understand how the aforementioned, data-driven, processes are making their way within the city, it is necessary to place under scrutiny the governmental structures within which they have been bred.

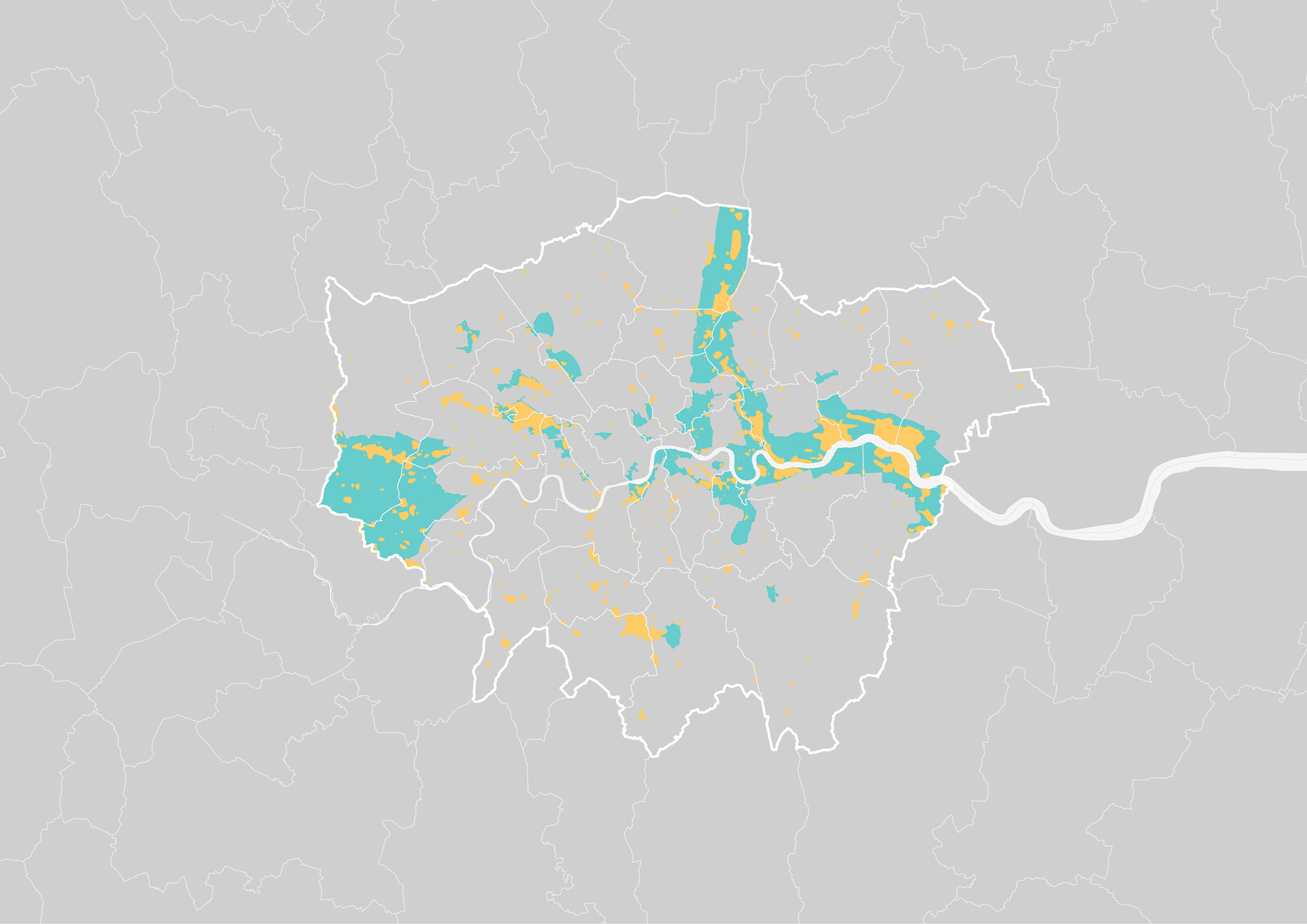

Map of London’s 37 Opportunity Areas (turquoise) and Industrial Lands (yellow), as designated by the Greater London Authority.

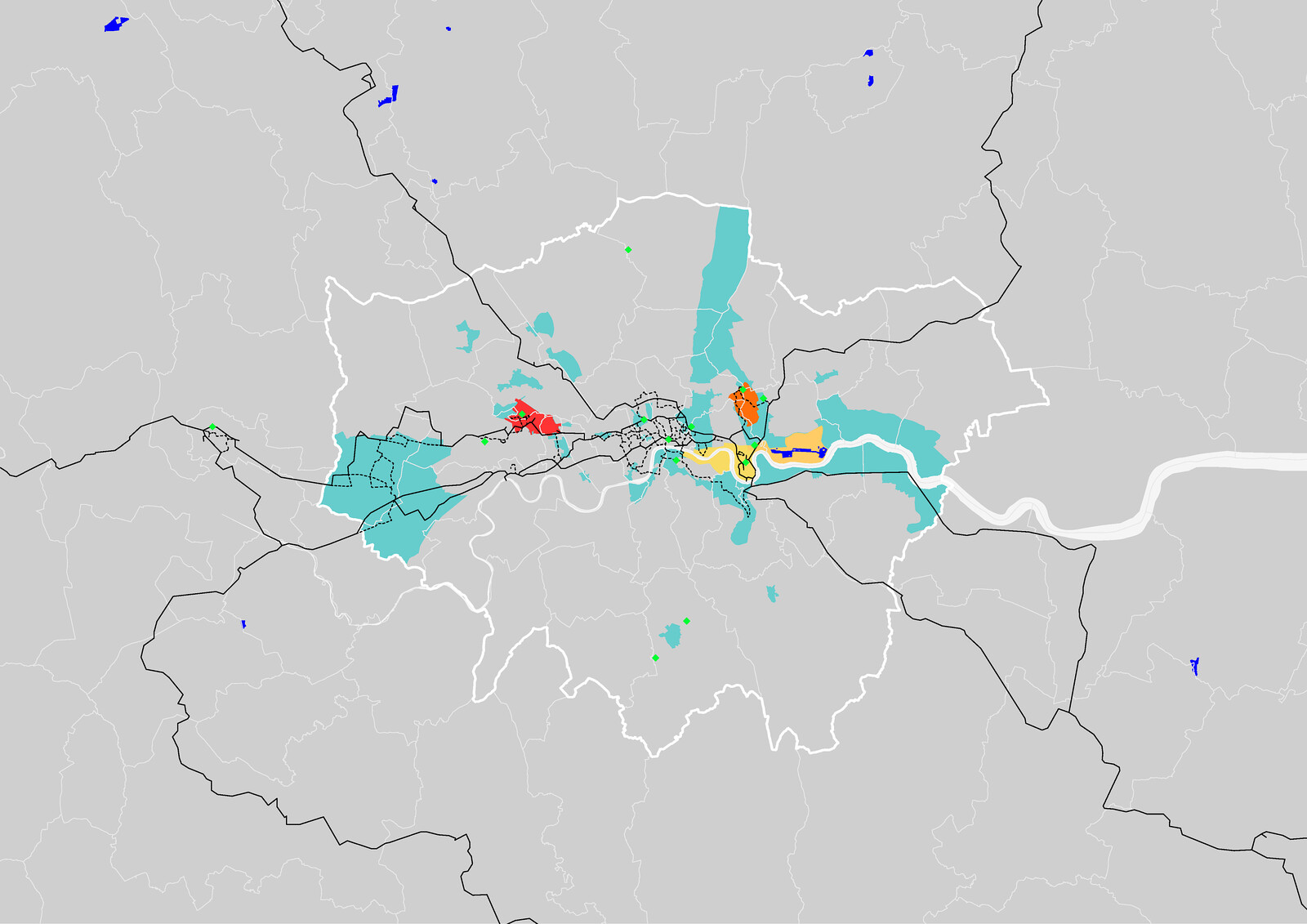

Map of London’s designated Opportunity Areas (turquoise), Enterprise Zones (blue), Long Haul Fiber Network (black), Metro Dark Fiber Network (dashed), and major data center hubs (green). Old Oak and Park Royal Development Corporation (2015–present), London Legacy Development Corporation (2012–present), and London Docklands Development Corporation (1981–1998) are also demarcated in red, orange, and yellow, respectively.

Map of London’s 37 Opportunity Areas (turquoise) and Industrial Lands (yellow), as designated by the Greater London Authority.

II.

Since the 2011 Localism Act and the consequent abolition of UK-wide Regional Strategies, London’s governance was subject to a series of rather seminal transformations in its mode of operation which would prove highly instrumental to the nurturing of a new urban economic model. Amongst these, the dissolution of the London Development Agency (LDA) was particularly significant in that the requirements of establishing London’s Economic Development and Environment Strategies now fell entirely in the hands of the Mayor. But the measures announced in the Localism Act had even greater implications in matters of planning, where the dissolution of regional frameworks meant that the decision making process would now be entirely subsumed in the relation between the Greater London Authority and its thirty-three local boroughs (including The City of London Corporation). In this, the GLA—a top-tier administrative body consisting of an elected mayor and assembly—would be responsible for coordinating land use planning through a strategic plan (the “London Plan”) which the boroughs—local authority districts governed by a homonymous council—would be legally bound to.

Although boroughs would have full control over submitted planning applications within their perimeters, the GLA retained power to override planning decisions made by democratically elected boroughs if they were believed to be against the interests of London as a whole.5 In essence, the GLA was given power to act as an inter-borough level of authority working within and between boroughs to drive integrated strategic planning policies through London’s fragmented and often conflictual governmental structure. Moreover, this newly gained power was buttressed by a whole other series of post-financial-crisis centralizing measures of exquisitely Thatcherite flavor. Amongst others, these provided City Hall with the possibility to define strategic “Opportunity Areas” (OAs) to drive policy and cross-borough issues that may prove contentious during the early stages of the planning processes (and thus risky for investors); the right to create trans-borough Mayoral Development Corporations run by (unelected) boards made-up of representatives from key political and business stakeholders that de facto replace local authorities for all planning matters (a revival of the 1980 Local Government Act); and the right to form Local Enterprise Partnerships between businesses, the Mayor and representatives of the boroughs to determine local economic priorities and lead economic growth.6 While sanctioning the further penetration of private interests into London’s political milieus, Local Enterprise Partnerships are all the more significant in that they can bid to create “Enterprise Zones,” wherein simplified planning procedures and business rate discounts are put in place to attract new, often international businesses.

The strategic nature of the areas, zones and corporations formed since 2012 in relation to the growing digitization of London’s economy is rendered all the more evident when measured against two further factors: the location of Strategic Industrial Land and the city’s data infrastructure. As far as the former is concerned, the 2015 London Industrial Land Supply & Economy Study highlights a clear correlation between the localization of Opportunity Areas, the establishment of Mayoral Development Corporations and the allocation of London’s residual industrial land for non-industrial uses (a reverberation of Thatcherite policy).7 Even more interesting though is the coincidental relation between the Long Haul and Metro Dark Fiber Networks trajectories and the location of major data storage facilities and the aforementioned areas, zones and corporations, the proximity between which essentially a) affirms their instrumentality as the very veins through which the industry’s blood flows, and b) demonstrates the indispensability of data infrastructure for contemporary real estate operations. Take, for instance, two recent Mayoral Development corporations: the London Legacy Development Corporation LLDC, which crosses the East London’s boroughs of Hackney, Tower Hamlets, Newham and Waltham Forest, has drafted a legacy plan for the site of London’s 2012 Summer Olympics, within which the Technology Cluster and Smart District is being developed by iCity, a joint venture between real estate investor Delancey and data center operator Infinity. West London’s Old Oak and Park Royal Development Corporation OPDC, which spans across Ealing, Brent, and Hammersmith & Fulham, is being given infrastructural carte blanche to develop ground-up strategies of smart-city technologies “within the very DNA of the forthcoming neighborhood.”8

III.

What we see with the privately managed data-driven governance apparatuses of London’s digital enclosures is the smart city standing within a line of development that began during the liberal agendas of the early 1980s. Indeed, it is not difficult to imagine how, in this Thatcherism 2.0, or “smart Thatcherism,” we are already assisting in the rise of even sharper inequalities than with its analogue predecessor—inequalities determined by proximity to data infrastructure just as much as transport infrastructure.9 In parallel, recent City Hall initiatives have pointed to an increasing reliance and politicization of big data and smart systems as urban decision making proxies. 2010 saw the launch of London Datastore—a web portal run by the GLA for sharing free open data and statistics about London to the public, businesses and academia—which led to the creation of more than 200 apps and many other data driven enterprises such as the public funded Open Data Institute (ODI). In 2013, “London Infrastructure Plan 2050” sanctioned the birth of the Smart London Board, through which a group of leading academics, businesses and entrepreneurs currently consult with and assist the Mayor on how to fully integrate smart technologies within the city’s infrastructure. The 2016 “Data for London. A City Data Strategy” publication saw the GLA essentially call for a radical process of data liberalization—not only of open data (as had occurred in 2010) but also private, commercial, sensory and crowd-sourced data—to foster further innovation in both the business sector and in city governance. With the progressive undoing of England’s Welfare State, the implementation of these initiatives and the likely machine-aided modes of government driven by quantifiable performance values which will arise from their implementation,10 are likely to cause further splintering of local authorities’ regulatory powers over the development of the contemporary productive landscape and of the civic space more broadly.11

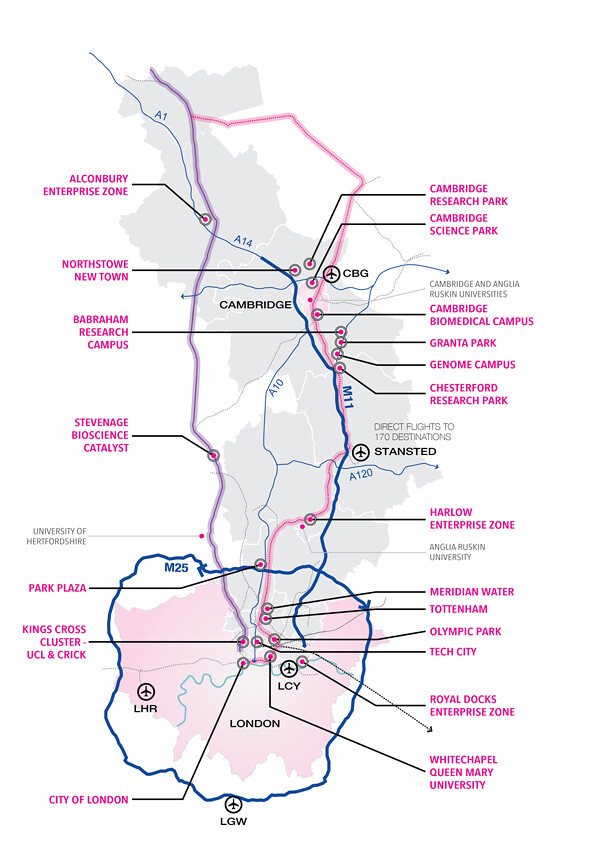

Map of Key Life Science Locations along the London-Stansted-Cambridge corridor. Source: LSCC

Moreover, key players in the Science and Technology sectors as much as larger political bodies are already tending to similar overarching powers of authority at the regional scale. The London Stansted Cambridge Consortium (LSCC) Growth Commission was recently established “in order to provide independent analysis and advice to raise economic potential … and set out a vision for transformational change” in a corridor spanning from Central London, through Stansted, up to Cambridge. Views of active investors in the LSCC have identified “the slow progress of Local Plans being prepared and adopted by the respective local authorities comprising the Corridor” as a key barrier to growth, “resulting in lower levels of confidence to invest in an area without an adopted strategy for future growth.”12 The challenge ahead, they argue, relies on an integrated planning framework enabling the region to compete at a global scale with established and upcoming innovation ecosystems. With reference to other areas of London where larger development corporations have superseded local planning authorities for planning matters, such as those aforementioned, the LSCC Growth Commission invokes the critical integration of metropolitan and regional planning powers to influence the concentration and distribution of growth and innovation between inner city areas and out-of-town development. If their visions were to be fulfilled, the agency of local authorities (and thus of local voters) would find itself even further weakened.

While typical top-down planning policies may not be sufficient to disrupt the polarization of growth and production given the current environment of “market realism,” what is clear is that, whether deliberately or not, the global “winner-takes-all urbanism” in its latest tech-based reincarnation is failing to confront itself with the economic and political consequences of the agglomerative and exclusive character of its spatial configurations.13 Furthermore, the case of London allows us to gauge with almost crystalline clarity the degree to which the revolutionary and democratic promises engendered by the digital “online” are, in fact, tightly knitted into the monetary frameworks, governmental means of sovereignty and infrastructural inequalities that characterized the urbanization of the free-market in the 1970s and 80s. As city administrators worldwide continue to cut long-term deals with global technology providers, it is unlikely that this model might be subverted in the long run. Open source softwares, the multiplication of ubiquitous information devices, wireless connectivity and the opportunity for city administrations to harness the potential of the continuous flow of data emitted by both citizens and cities at all times without recurring to proprietary technologies, might indeed offer concurrent solutions to the despotism of private companies in determining their and our future.14 Yet the true challenges we face today are ultimately political much more than they are technological, and that the problems brought about by the digitization of our urban landscapes cannot but be addressed without reforming the governmental and legal structures within which they are brought to bear. Whether London’s current Labor mayorship will come to terms with this reality, remains an open question.

To name a few: the London Legacy Development Corporation appointed iCity, a 2012 joint venture between real estate investor Delancey and data center operator Infinity to redevelop a part of the Olympic Park into the UK’s largest Technology Center and Smart district; the 2016 TMRW Technology Hub in the borough of Croydon which was born supported by dedicated Regeneration and Enterprise Funding, tax reliefs and a rent and rate free period from the local council; City Hall’s 2010 London Datastore, a web portal run by the GLA for sharing free open data and statistics about London with the public, businesses and academia leading to the creation of more than 200 apps and many other data driven enterprises such as the public funded Open Data Institute (ODI); the 2013 “London Infrastructure Plan 2050” and the birth of the Smart London Board, through which a group of leading academics, businesses and entrepreneurs currently consult with and assist the Mayor on how to fully integrate smart technologies within the city’s infrastructure; the 2016 “Data for London. A City Data Strategy” publication in which the GLA essentially calls for a radical process of data liberalization, not only of open data (as had occurred in 2010) but also private, commercial, sensory and crowd-sourced data to foster further innovation in both the business sector and in city governance. This latter strategy is underway of implementation in the current Opportunity Area (OA) and former industrial site of Old Oak and Park Royal where, by commission of the homonymous Development Corporation, a preliminary “Smart Strategy” was delineated by the Hypercat consortium to “embed smart city technology and approaches within the very DNA of the forthcoming neighborhood.”

According to a report commissioned from SQW and Trampoline Systems, there are 90,000 science and technology (S&T) businesses in London that employ approximately 700,000 people. The report also highlights the capital’s fifty incubators, accelerators and innovation centers that have developed over recent years. It also identifies the significance of London’s universities and the presence of major teaching hospitals and academic health science centers.

By fiber we mean the metropolitan fiber optic networks through which data travels.

Andrew Blum, Tubes (London: Penguin Books Ltd, 2012), 189-197.

For instance, Mayor B. Johnson submitted the order that any “development which comprises or includes the erection of a building or buildings … (c) … outside Central London and with a total floorspace of more than 15,000 square meters,” and any “development which comprises or includes the erection of a building of…(c)…more than 30 meters high and is outside the City of London” should be submitted to the GLA for assessment.

“The London Economic Action Partnership (LEAP) is the local enterprise partnership for London. The LEAP brings entrepreneurs and business together with the Mayoralty and London Councils to identify strategic actions to support and lead economic growth and job creation in the capital.” See ➝.

While residential property values in East London have exponentially risen, market pressures to develop London’s stock of land have radically modified the urban ecosystem into a residential mono-culture, polarized between high growth areas in inner London and sprawling warehouse development in outer boroughs. An attempt by the GLA to challenge this monoculture affirming the growing demands in data storage and logistics is its consideration to implement land use categories dedicated to “Storage and Distribution” upon Strategic Industrial Land sites. In the Town and Country Planning use classes, ‘storage and distribution’ falls under the category B8 which includes clean-tech processes such as data storage facilities and “mid-tech” buildings—i.e. hybrid warehouses and office space.

This is currently one of the largest regeneration projects in the whole of the UK counting a total of over 650 hectares in footprint, the provision of 55,000 jobs and an expected development of 24,000 homes. It also amounts to the largest industrial land in greater London and the only site HS2 and Crossrail intersect. The OPDC board includes bodies as disparate as the Ealing Council, Network Rail, Brent Council, Hammersmith and Fulham Council, Park Royal Business Group, Imperial College London, Outer London Commission, High Speed 2, Residents Association. The area’s Smart Strategy has been drafted by the Development Corporation in collaboration with Hypercat, a not for profit organization driving secure and interoperable Internet of Things (IoT) for industry and cities. See ➝. In both instances, Long Haul and Dark Fiber networks have been designed to loop within their boundaries, ensuring high speed connectivity to future businesses and data storage facilities.[footnote Within London, Long Haul Networks refer to dedicated bandwidth services across Pan European fibre cables offered from network owners and operators (such as EUnetworks, Venus, Interoute) to businesses in need of exchanging data across Europe at low latency and with reliable connectivity (ie finance and media). Metro Dark Fibre Networks refer to metropolitan “dark” or “unlit” fibre cables networks (ie not yet occupied) that can be leased in their entirety to a single business or organisation to guarantee full control, speed and scalability of their private data network.

SQW “Mapping London’s Science and Technology Sectors” (2015), ➝, highlights how the processes of clustering (co-location of similar businesses) and agglomeration (spatial proximity of different factors such as connectivity, access to finance and cross-sectoral fertilization) at the very foundation of London’s successful integration of the digital economy within its city-space is further increasing the capital’s chronic issues of high housing costs, transport congestion and inequality, in turn described as key limits to future growth and socio-economic integration. This dilemma is further exemplified by two key findings extracted from the SQW report: the first one relates to employment throughout London across the last ten years and shows that while jobs in “digital technologies” increased by 29%, the number in “other scientific/technological manufacture” decreased by 45% signaling the decline of urban manufacturing sectors and the consolidation of digitally enabled businesses with a skilled workforce. The second one considers employment distribution by sector across London’s geography and shows that while technology jobs increased by 29% in Inner London, employment within the same sectors decreased by 6% in Outer London Boroughs. Geographical differences within London’s boundaries are even spikier if considering the “digital technologies” sector, which saw a 53% increase in Inner London (City of London, Camden, Greenwich, Hackney, Hammersmith and Fulham, Islington, Kensington and Chelsea, Lambeth, Lewisham, Newham, Southwark, Tower Hamlets, Wandsworth, and Westminster) and a fall of 4% in Outer London (Barking and Dagenham, Barnet, Bexley, Brent, Bromley, Croydon, Ealing, Enfield, Haringey, Harrow, Havering, Hillingdon, Hounslow, Kingston upon Thames, Merton, Redbridge, Richmond upon Thames, Sutton and Waltham Forest).

Addressing London’s future City Data Market, the Greater London Authority’s lead officer on the Smart Cities Agenda Andrew Collinge has declared: “We want to make it abundantly clear that this City Hall does not have the expertise and indeed resources to tackle the issues – from data security to privacy to monetization and harmonization – thrown up by our City Data Strategy. We doubt anyone does. Finding those answers means adopting a collaborative and wholly open approach with business, academia and Londoners – anyone who possesses data talent. We firmly believe though that we are taking a step in the right direction. We are innovating by giving a deterministic focus on using city data to pursue (market) opportunities that equate to more than the demand we can induce through plain procurement. In a new definition of City Data, we are giving extra focus to what sort of data, and whose data should be used – either open if we can but in a secure shared environment if needs be – in pursuit of answering city challenges. Our work on city data and ‘smart’ is changing the way that London’s government sees technology as part of the solution for the city’s challenges. There is a high likelihood that the new Mayor will appoint a Chief Digital Officer to promote new technology solutions and to make data work to maximum effect across the critical policy areas of housing, transport, cybercrime, and the environment.” See ➝.

If one were to extend the concept of splintering urbanism—described by Stephen Graham and Simon Marvin, in Splintering Urbanism: Networked Infrastructures, Technological Mobilities and the Urban Condition (London: Routledge, 2001) as “the fragmentation of the social and material fabric of cities caused by the relegation of urban infrastructure networks and the mobilities they support”—to today’s data deluge we would notice how the multiplication of ubiquitous information devices (smart phones, Internet of Things) and wireless connectivity (4G, 5G) is contributing to the creation of a new form of infrastructure that corresponds to the continuous and unstructured flow of data emitted by cities at all times.

Nathaniel Lichfield & Partners, London Stansted Cambridge Corridor Growth Commission: Understanding Potential (London: 2016).

cf. Richard Florida, The New Urban Crisis: How Our Cities Are Increasing Inequality, Deepening Segregation, and Failing the Middle Class and What We Can Do about It (New York: Basic Civitas Books, 2016).

See the work of Mara Balestrini (Ideas for Change) as technology strategist for the city of Barcelona, ➝.

Post-Internet Cities is a collaborative project between e-flux Architecture and MAAT – Museum of Art, Architecture and Technology within the context of the Utopia/Dystopia exhibition and “Post-Internet Cities” conference, produced in association with Institute for Art History, Faculty of Social Sciences and Humanities – Universidade NOVA de Lisboa and Instituto Superior Técnico – Universidade de Lisboa, and supported by MIT Portugal Program and Millennium bcp Foundation.

Category

Post-Internet Cities is a collaborative project between e-flux Architecture and MAAT – Museum of Art, Architecture and Technology within the context of the Utopia/Dystopia exhibition and “Post-Internet Cities” conference, produced in association with Institute for Art History, Faculty of Social Sciences and Humanities – Universidade NOVA de Lisboa and Instituto Superior Técnico – Universidade de Lisboa, and supported by MIT Portugal Program and Millennium bcp Foundation.